Introduction: The New Axis of Global Growth

For decades, global growth discussions centered on the United States, Europe, and Japan. Today, that conversation increasingly shifts eastward — toward China and India.

Both countries are projected to remain among the largest contributors to global GDP expansion over the next decade. Yet they represent fundamentally different economic models.

China is a mature industrial powerhouse navigating structural moderation.

India is a rising consumption-driven economy benefiting from demographic momentum.

The comparison is not about which country “wins.” It is about how global growth will be distributed across two very different trajectories.

Scale Versus Speed

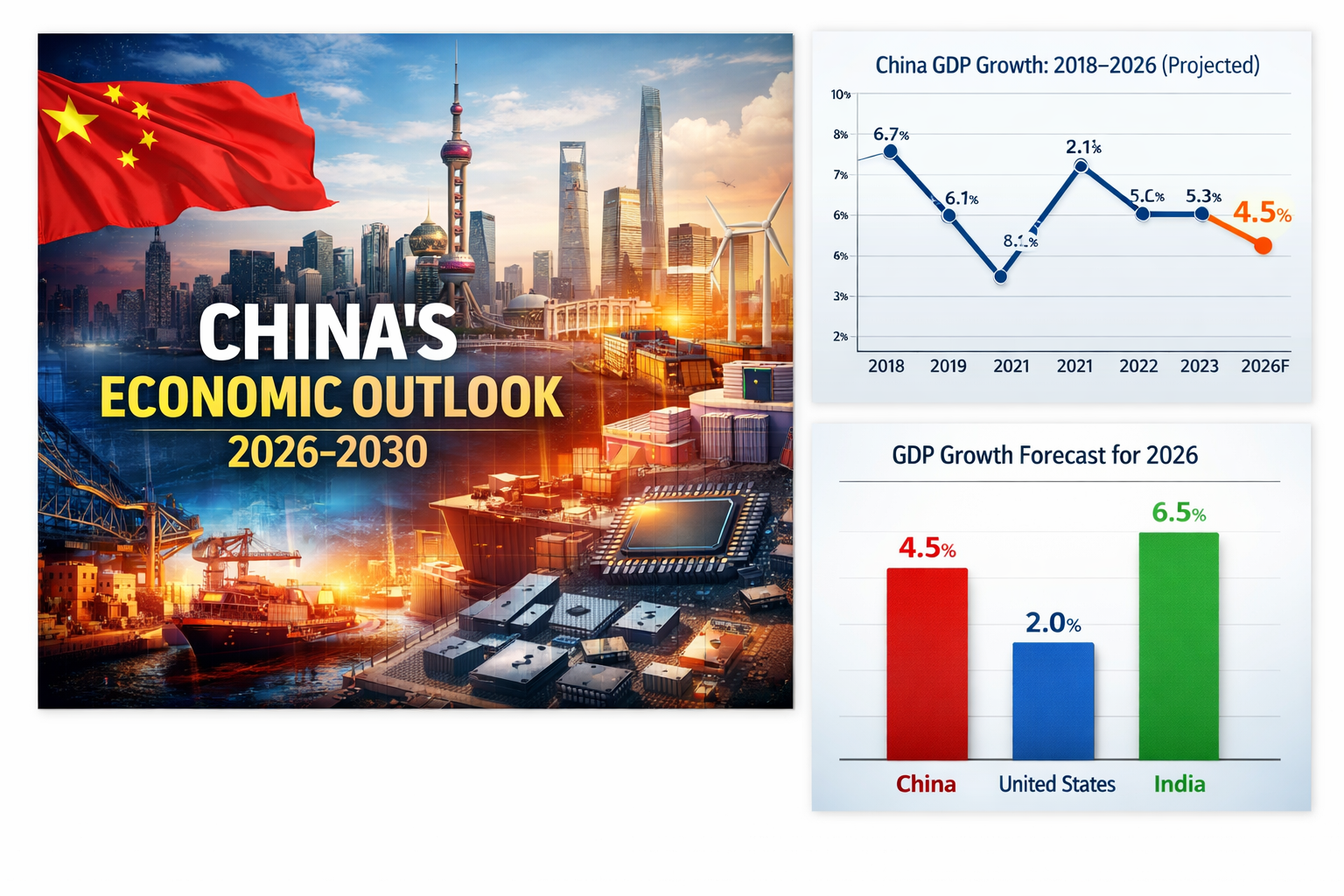

India’s projected annual growth rate of 6–7% exceeds China’s expected 4–5% medium-term expansion. At first glance, this suggests India is overtaking China.

But scale changes interpretation.

China’s economy is more than five times larger than India’s in nominal terms. Even at lower percentage growth, China may still add more absolute output annually than India.

A useful distinction emerges:

- India represents higher percentage growth.

- China represents higher absolute economic contribution.

Both matter. But they operate differently.

For context on China’s structural trajectory, see our full analysis:

China’s Economic Outlook 2026–2030.

{kind=link}

Demographics: India’s Structural Advantage

India’s population profile provides a tailwind. A younger workforce, expanding labor participation, and urbanization create conditions for sustained domestic demand growth.

China, by contrast, faces workforce contraction and aging pressures. Its demographic dividend has largely passed.

However, demographic advantage only translates into growth if employment generation and productivity keep pace. Labor force expansion without sufficient job creation does not guarantee prosperity.

The coming decade will test whether India can convert demographic potential into consistent capital formation and manufacturing depth.

Industrial Ecosystems and Infrastructure Depth

China’s comparative strength lies in industrial integration.

Decades of infrastructure buildout, export orientation, and supply chain clustering have created ecosystems that are difficult to replicate quickly. From advanced electronics to electric vehicle production, China retains logistical and technological advantages.

India is expanding its industrial capacity through production-linked incentives and infrastructure investments. But ecosystem depth takes time. Manufacturing scale is not built overnight.

In the near term, China anchors global industrial output. India is accelerating — but still building.

The Structural Outlook

The most realistic scenario for 2026–2035 is not replacement but coexistence:

- China stabilizes as a mature industrial growth engine.

- India expands as a high-growth consumption and services hub.

Together, they may define the next chapter of emerging market expansion.

The global system increasingly depends on both.